WHAT DID THE FED ANNOUNCE ON WEDNESDAY?

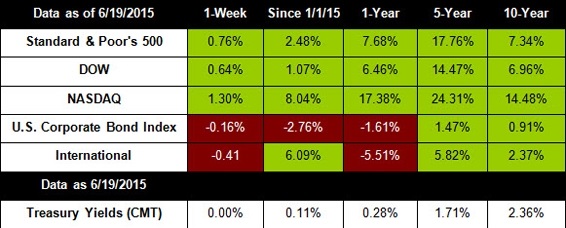

Last week, markets shrugged off concerns about deadlocked Greek negotiations and rallied on strong economic data, sending the NASDAQ to a new historic high. For the week, the S&P 500 grew 0.76%, the Dow rose 0.64%, and the NASDAQ gained 1.30%.[1]

The Federal Reserve wrapped up its June meeting on Wednesday surprising no one with the announcement that the central bank will keep rates at zero percent for a while longer. Though the Fed appears to be confident that the economy is growing modestly, officials prefer to maintain the status quo until they’re more certain that rate hikes won’t harm the recovery.[2]

We don’t yet know when the Fed will begin raising interest rates, but a number of respondents to a recent survey are betting on a third-quarter rate hike.[3] Are rate expectations already baked into stock and bond markets? It’s hard to know for certain, but the Fed has been doing a good job of laying the groundwork for future rate moves, so we can hope that markets won’t overreact when rates start to go up.

Negotiations between Greece and its European lenders broke down again Thursday, weighing on European stocks. Greece is trying to negotiate a new round of credit from European lenders that would allow it to make scheduled debt repayments by the end of June. Negotiators have not been able to reach a deal that would satisfy creditors’ need for budget cuts and pension reform. Though Thursday’s meeting was billed as a last-chance effort to break the deadlock, some time remains before Greece formally falls into default.[4] How will the game of chicken end? We don’t know.

Looking ahead, European and Greek leaders will hold an emergency summit on Monday to attempt to resolve the bailout gridlock. Panicked about what would happen if Greece defaults on its debt payments and leaves the Eurozone, depositors have been withdrawing cash from Greek banks, leaving some insiders speculating that Greek banks may not be able to reopen next week. If negotiators are unable to reach a compromise before the end of the month, we can expect the breakdown to cause markets to turn volatile. We’ll keep you updated as necessary.

ECONOMIC CALENDAR:

Monday: Existing Home Sales

Tuesday: Durable Goods Orders, PMI Manufacturing Index Flash, New Home Sales

Wednesday: GDP, EIA Petroleum Status Report

Thursday: Jobless Claims, Personal Income and Outlays

Friday: Consumer Sentiment

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance and Treasury.gov. International performance is represented by the MSCI EAFE Index. Corporate bond performance is represented by the DJCBP. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

HEADLINES:

Housing starts fall in May. Groundbreaking on new houses fell last month, but a surge in permits for new construction suggests that the pause may be temporary and that the housing sector will see strong growth this season.[5]

Jobless claims fall more than expected. The number of Americans filing new claims for unemployment benefits fell more than expected, remaining below the key 300,000 level for the 15th week in a row.[6]

Inflation sees biggest gain in two years. Consumer prices jumped in May by the largest amount since 2013. The data indicates that price drops relating to gasoline savings may be over and that inflation is returning to trend.[7]

Apartment rentals reach historic high. Occupancy rates in apartments reached 95.3% in May, the highest level on record, as Americans of all ages move into rental housing in droves.[8]

These are the views of Platinum Advisor Marketing Strategies, LLC, and not necessarily those of the named representative, Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indexes from Europe, Australia and Southeast Asia.

The Dow Jones Corporate Bond Index is a 96-bond index designed to represent the market performance, on a total-return basis, of investment-grade bonds issued by leading U.S. companies. Bonds are equally weighted by maturity cell, industry sector, and the overall index.

The S&P/Case-Shiller Home Price Indices are the leading measures of U.S. residential real estate prices, tracking changes in the value of residential real estate. The index is made up of measures of real estate prices in 20 cities and weighted to produce the index.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Google Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

- https://www.google.com/financechdnp

- http://www.cnbc.com/id/102766785

- http://www.reuters.com

- http://www.cnbc.com

- http://www.foxbusiness.com/

- http://www.foxbusiness.com/

- http://www.foxbusiness.com/

- http://www.cnbc.com/

The information presented is for educational purposes only and should not be considered personalized investment, tax, or legal advice.